My ratings on ETFs are unique because they are based on my stock ratings for each of a fund’s holdings.

Analyzing and rating an ETF based on its holdings delivers many interesting insights:

- The size of the allocation to each holding is most important to the predictive rating of the ETF.

- The largest holdings are not reliable indicators of quality or investment merit.

- ETF labels/names are not reliable indicators of quality or investment merit.

Figures 1 and 2 prove these points.

First, note that none of the overall top-rated ETFs (in Figure 1), all of which get my Attractive fund rating, rank in the top 10 of the ETFs (in Figure 2) with the largest allocations to stocks in my monthly Most Attractive Stocks newsletter, which is ranked as one of the best model portfolios in the business by Barron’s.

Figure 1: Top 10 Rated ETFs

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

It is natural to assume that the ETFs with the largest allocations to my Most Attractive Stocks, my top-rated stocks, would be my top-rated ETFs. In reality, none of the ETFs with the largest allocation to the Most Attractive Stocks (Figure 2) make the list of top-rated ETFs (Figure 1). They are close, but not good enough because their allocations to Neutral-or-worse rated stocks exceed the allocations to the Most Attractive stocks.

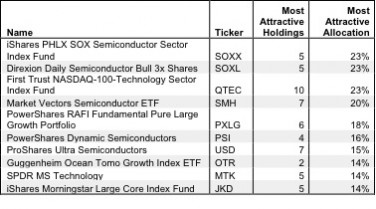

Figure 2: Top 10 ETFs With Largest Allocations to Most Attractive Stocks

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

Further, only three of the ETFs in Figure 2 get an Attractive rating, the rest are Neutral despite having the largest allocations to the Most Attractive Stocks. Ratings and reports on all the ETFs in Figures 1 and 2 are here.

Clearly, the large allocation to good stocks, ie. the Most Attractive Stocks, does not necessarily translate into a good rating. One cannot trust the largest holdings to be representative of the ETF.

For example, PowerShares Dynamic Semiconductors (PSI) allocates 16% (ranks 6th out of all ETFs I cover) to stocks on the Most Attractive Stocks list. Each of its top 5 holdings, which represent over 25% of the ETF, gets my Very Attractive or Attractive rating. However, this ETF gets my Neutral rating because it allocates over 50% of its portfolio to stocks that get my Neutral or Dangerous rating. My report on PSI has the details.

Takeaway: proper due diligence on an ETF requires research on ALL of the ETF’s holdings. The largest holdings typically represent only a small fraction of the overall portfolio. The quality of the smaller holdings, in aggregate, usually has a meaningful impact on the overall quality of the portfolio.

Lastly, do not judge an ETF by its name, type or label. Figures 1 and 2 show that ETFs of all types make both of my top 10 lists. Conversely, all types of ETFs are also on my bottom 10 lists.

True, there are more Semiconductor/Technology ETFs in Figures 1 and 2 than any other category. However, as detailed in my Best & Worst funds series, every category of ETF has both bad and good ETFs, with rare exception.

One of the stocks that shows up consistently in the technology ETFs is Apple [s: AAPL]. This stock gets my Very Attractive rating, and at 270%, it has the highest return on invested capital (ROIC) of any large cap stock in the US markets and, probably, the world.

Many people see AAPL as an expensive stock given its impressive appreciation recently. They are missing the elite level of profitability the company has achieved. With an ROIC of 270%, the company is generating $2.70 for every dollar of capital in the business. When a business is as profitable as AAPL, it requires very little top line growth to drive much larger profit growth.

For example, to justify a $600 stock price, the company needs only to grow at 15% for two years. If you believe, as I do, the company can do better than that, then the stock is cheap. My AAPL report offers the details on my ROIC and DCF calculations.

See my free stock screener for my ratings on 3000+ stocks updated daily.

Disclosure: I own AAPL. I receive no compensation to write about any specific stock, sector or theme.