This report identifies the “best” ETFs and mutual funds based on the quality of their holdings and their costs. As detailed in “Low-Cost Funds Dupe Investors”, there are few funds that have both good holdings and low costs. While there are lots of cheap funds, there are very few with high-quality holdings.

Without speculating on the cause for this disconnect, I think it is fair to say that there is a severe lack of quality research into the holdings of mutual funds and ETFs. There should not be such a large gap between the quality of research on stocks and funds, which are simply groups of stocks.

After all, investors should care more about the quality of a fund’s holdings than its costs because the quality of a fund’s holdings is the single most important factor in determining its future performance.

My Predictive Rating system rates 7400+ mutual funds and ETFs according to the quality of their holdings (portfolio management rating) and their costs (total annual costs rating).

The following is a summary of my top picks and pans for all style ETFs and mutual funds. I will follow this summary with a detailed report on each style, just as I did for each sector.

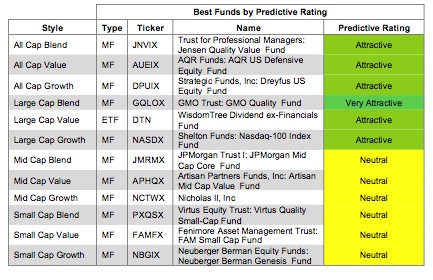

Figure 1 shows the best ETF or mutual fund in each investment style as of January 31, 2013. Note that the only style containing a Very Attractive rated fund is the Large Cap Blend style.

For a full list of all ETFs and mutual funds for each investment style ranked from best to worst, see our free ETF and mutual fund screener.

Figure 1: Best ETFs and Mutual Funds In Each Style

Source: New Constructs, LLC and company filings

Source: New Constructs, LLC and company filings

GMO Trust: GMO Quality Fund (GQLOX) is our highest rated fund in any style. It doesn’t allocate any assets to Dangerous or worse rated funds, and it has a low total annual cost of 0.51%.

Oracle Corporation (ORCL) is one of my favorite stocks held by GQLOX and earns our Very Attractive rating. Oracle has a truly impressive NOPAT CAGR of 18% over the last 10 years. Despite this fact, Oracle’s stock, ~$35.38/share, trades at a price to economic book value ratio of only 1.0. This ratio implies zero growth in NOPAT in the future. If ORCL continues to grow NOPAT at all, investors should see that share price go up.

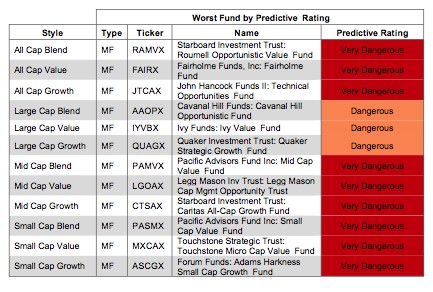

Figure 2 shows the worst ETF or mutual fund for each investment style as of January 31, 2013.

Dangerous-or-worse-rated funds have a combination of low-quality portfolios (i.e. they hold too many Dangerous-or-worse rated stocks) and high costs (they charge investors too much for the [lack of] management they provide).

Figure 2: Worst ETFs and Mutual Funds In Each Style

Source: New Constructs, LLC and company filings

Source: New Constructs, LLC and company filings

Pacific Advisors Fund Inc: Small Cap Value Fund (PASMX) is our worst rated ETF or mutual fund for any style and earns our Very Dangerous rating. PASMX allocates 69% of its assets to Dangerous or worse rated stocks and, on top of that, charges investors annual costs of 5.60%.

Conn’s Inc. (CONN) is one of my least favorite stocks held by PASMX and earns our Dangerous rating. CONN’s share price more than doubled last year. This growth was not backed up by any change in return on invested capital (ROIC), which rose by only 0.2%. Such an unsubstantiated price should make investor wary. CONN’s current valuation of ~$27.55 per share implies NOPAT growth of 17% compounded annually over the next 18 years. Investors would be wise not to bet on such dramatic growth.

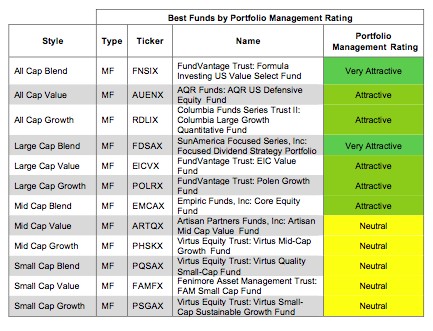

Traditional mutual fund research has focused on past performance and low management costs. The quality of a fund’s holdings has been ignored. Our portfolio management rating examines the fund’s holdings in detail and takes into account the fund’s allocation to cash. Our models are created with data from over 40,000 annual reports. This kind of diligence is necessary for understanding just what you are buying when you invest in a mutual fund or an ETF.

Figure 3 shows the best fund based on our Portfolio Management Rating for each investment style as of January 31, 2013.

Attractive-or-better-rated funds own high-quality stocks and hold very little of the fund’s assets in cash – investors looking to hold cash can do so themselves without paying management fees. Only 6.3% of funds receive our Attractive or Very Attractive ratings, so investors need to be cautious when selecting a mutual fund or ETF – there are thousands of Neutral-or-worse-rated funds.

Figure 3: Style Funds With Highest Quality Holdings

Source: New Constructs, LLC and company filings

Source: New Constructs, LLC and company filings

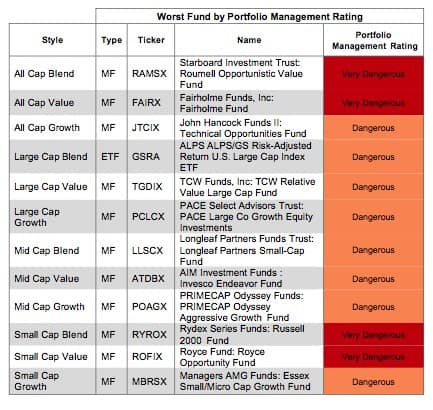

Figure 4 shows the worst fund based on our Portfolio Management Rating for each investment style as of January 31, 2013.

Investors pay mutual fund managers to pick stocks for them. Even ignoring costs, these mutual fund managers do a poor job investing money for their clients.

Figure 4: Style Funds With Lowest Quality Holdings

Source: New Constructs, LLC and company filings

Source: New Constructs, LLC and company filings

Investors should care about all of the fees associated with a fund in addition to the quality of the fund’s holdings. The best funds have both low costs and quality holdings – and there are plenty of low cost funds available to investors.

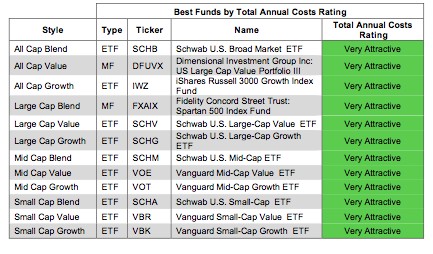

Figure 5 shows the best fund in each investment style according to our total annual costs rating. An ETF ranks as the lowest cost for seven of the twelve style categories.

Total Annual Costs incorporates all expenses, loads, fees, and transaction costs into a single value that is comparable across all funds. Passively managed ETFs and index mutual funds are generally the cheapest funds.

The number of funds with Very Attractive total annual costs rating shows that it is much easier to find funds with low costs than it is to find funds with quality holdings.

Figure 5: Style Funds With Lowest Costs

Source: New Constructs, LLC and company filings

Source: New Constructs, LLC and company filings

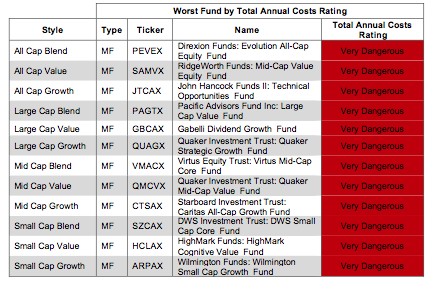

The most expensive fund for each investment style has a Very Dangerous Total Annual Costs Rating. Investors should avoid these funds and other funds with a Very Dangerous Total Annual Costs Ratings because they charge investors too much. For every fund with a Very Dangerous Total Annual Costs Rating there is an alternative fund that offers similar exposure and holdings at a lower cost. We cover over 7000 mutual funds and over 400 ETFs. Investors have plenty of alternatives to these overpriced funds.

Figure 6 shows the worst fund in each investment style according to our total annual costs rating. No ETFs ranks as the most expensive for any style category.

Figure 6: Style Funds With Highest Costs

Source: New Constructs, LLC and company filings

Source: New Constructs, LLC and company filings

Sam McBride contributed to this report.

Disclosure: David Trainer owns ORCL. David Trainer and Sam McBride receive no compensation to write about any specific stock, sector or theme.