Earlier this week, I wrote about how the pressure to innovate and the increasing competition makes Apple’s extraordinarily high return on invested capital (ROIC) unsustainable. Innovations can bring in massive profits for a brief time, but those profits invite competition and copycats, which, eventually, drive down profits and margins. No company can stay on the leading edge of innovation forever.

Profiting From Disruptive Innovation

My favorite aspect of Accenture’s (ACN) business model is that it profits from others’ innovations without having to incur the costs and pressures of innovation, itself. By establishing itself as the go-to name in IT and management consulting, Accenture has the potential to bring in new business with every major disruptive innovation, regardless of where that innovation comes from and with little R&D spending of its own.

In The Innovators Dilemma, Clayton Christensen explains how companies that do everything right can still struggle when disruptive innovation changes the market. The leaders at Accenture have clearly read this book, as the company excels at identifying new, high growth markets brought about by disruptive innovations.

For example, Accenture developed cloud solutions for its customers. Its Cloud Platform and more than 6,700 cloud experts brought in $1 billion in revenue last year, a promising sign for an industry as a whole has been growing by more than 27% compounded annually.

In addition, Accenture’s holistic view towards serving its clients has allowed it to achieve an impressive diversity in its business. Recently it has significantly grown its digital marketing division, landing contracts from BMW earlier this month. Like cloud computing, digital marketing is a rapidly growing business, with industry revenues growing by 15% in 2012. Not many companies can offer highly technical cloud support and a creative advertising campaign at the same time. Accenture’s diverse capabilities differentiate it from its competitors.

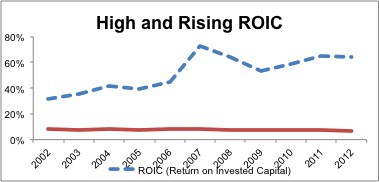

Figure 1: Widening the Gap Between Returns and Costs

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

Human Capital Is A Competitive Advantage

Much of Accenture’s success comes from its ability to identify and hire the best talent in different fields of expertise. The company’s high-quality personnel enable it to offer better solutions to a wider range of clients.

Accenture faces plenty of competition from companies like IBM and its Global Business Services unit, but the quality of Accenture’s people enables it to remain the leader in consulting. This strategy is self-perpetuating. Accenture is like a college football dynasty: the best high school recruits want to play for the best college programs, and the best young consultants want to work at the best consulting firm, Accenture.

Consistent Track Record of Profitability

The quality of Accenture’s strategy manifests in its profitability. ROIC is a key indicator of management’s ability to create value for shareholders, and Accenture has had a high and growing ROIC for the past decade. Figure 1 shows Accenture’s ROIC versus its weighted average cost of capital (WACC) over the past 10 years.

The 30% ROIC that Accenture had 10 years ago is exceptional. The fact that it has more than doubled its ROIC since then is a testament to its high quality management. Few firms can sustain those kinds of returns, but I think Accenture has the ability to do so. In 2012, its asset write-downs totaled only 3.5% of its total net assets, a sign that the company wastes very little of its invested capital. As long as management continues to allocate capital efficiently, Accenture’s advantages in quality and diversity of services should allow it to maintain its high returns.

More recent data also reflects brightly for the outlook on Accenture. Accenture grew its net operating profit after tax (NOPAT) by 18% in 2011 and 12% last year. Its IT consulting division significantly outperformed IBM’s last year, as revenue for IBM Global Business Services declined by 2% in 2012.

No matter what time range I review, Accenture’s history attests to the quality of its management and business model.

Priced for Stagnation

Despite its impressive fundamentals and strong track record of growth, ACN is priced like a company with almost no growth potential. At its current valuation of ~$80.76, ACN has a price to economic book value ratio of 1.11, implying that it will never grow NOPAT by more than 11% from its current level for the remainder of its corporate life. Contrast this modest expectation with ACN’s NOPAT compound annual growth rate of 12.6% over the last 10 years.

There does not appear to be any reason to expect ACN’s growth to slow down so drastically. If anything, the increasingly high-tech economy and the growth of “big data” should increase the demand for ACN’s services. On the balance sheet, ACN’s $5.2 billion in excess cash more than covers its liabilities, meaning investors don’t have to worry about future cash flows being significantly diverted to pay off debts or underfunded pension plans.

It’s rare to find a global leader in a growing and stable business with almost no growth built into the stock price. Investors should take advantage of the chance to buy such a solid company at a cheap price.

For investors who prefer their exposure to ACN to come through a mutual fund or ETF, I recommend Advisers Investment Trust: Independent Franchise Partners US Equity Fund (IFPUX) due to its 5.3% allocation to ACN and Attractive rating.

Sam McBride contributed to this report.

Disclosure: David Trainer owns ACN. David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.