Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life and MarketWatch.com.

Zynga (ZNGA) is in the Danger Zone this week. The stock has been beat up since its much-hyped IPO in 2011, but even after losing 61% of its value the stock is still too expensive. ZNGA is competing in an immature market where the barriers to entry are almost nonexistent and brand loyalty is a foreign concept. In addition, the company is bleeding cash and has hidden liabilities on its balance sheet. Investors have celebrated new CEO Don Mattrick from Microsoft (MSFT), but he will have to be quite the miracle maker to justify the celebration.

Weak Competitive Position

Most of the optimism for ZNGA came from the fact that it was a large player in a growing industry. The problem with the social and mobile gaming industry is that past success is not a great predictor of future success. Just because ZNGA has had hit games like FarmVille and Words With Friends does not mean it will make any money or even continue to produce popular games.

Investors need to recognize the difference between social/mobile games and console games. Console game developers can develop brand loyalty and churn out several installments of successful franchises such as Electronic Arts (EA) with FIFA and Madden and Activision Blizzard (ATVI) with Warcraft. ZNGA cannot rely on brand loyalty or build long-term franchises in the short-attention-span world of mobile games. It has to constantly produce original games to keep users’ attention.

Making matters worse, predicting what games will be successful in mobile gaming is nearly impossible. One year ago, very few people had heard of mobile developer King. Now, its game Candy Crush Saga is the top grossing game on Facebook and the company just filed for an IPO at a rumored valuation of $5 billion. With almost no barriers to entry and minimal economies of scale, Zynga’s business model is under constant threat of other companies stealing market share.

Profits? We talking about profits?!?…

When analyzing companies like Zynga (and several other Danger Zone picks such as Tesla (TSLA) and Linked In (LNKD)) whose market values seem preposterously high compared to their profits, I am reminded simultaneously of my experience at Credit-Suisse (CS) during the tech bubble and Allen Iverson’s timeless dismissal of the importance of “practice”.

On top of all the competitive pressures listed above, ZNGA makes no profit. That is right…we are talking about no profits or near-term expectations for profits for a $2.9 billion market cap company. Smells like a tech bubble valuation to me.

Mobile game developers have had limited success selling upgrades and premium content within free games, and many consumers have pushed back against this practice. The more ZNGA tries to lure gamers to make in-game purchases, the more it risks alienating its consumers and pushing them to other developers.

With a partner like Facebook (FB), who needs competitors? As Facebook’s (FB) policies have become less favorable to game developers, ZNGA has focused more on pure mobile games. However, the Facebook platform still accounted for 86% of ZNGA’s revenue in 2012, so the company remains vulnerable to further policy shifts by the social media giant.

Analysts briefly touted the possibilities of online gambling for ZNGA, but the company has decided to forego that route.

It is not clear from where the profits will come or that they will be sustainable if they do materialize.

Red Flags Hidden in the Footnotes

Everyone knows that ZNGA is not currently making money. However, many investors probably missed some of the accounting tricks that help ZNGA minimize its losses and hide its liabilities. Our analysis of ZNGA’s 2012 Form 10-K turned up a number of red flags:

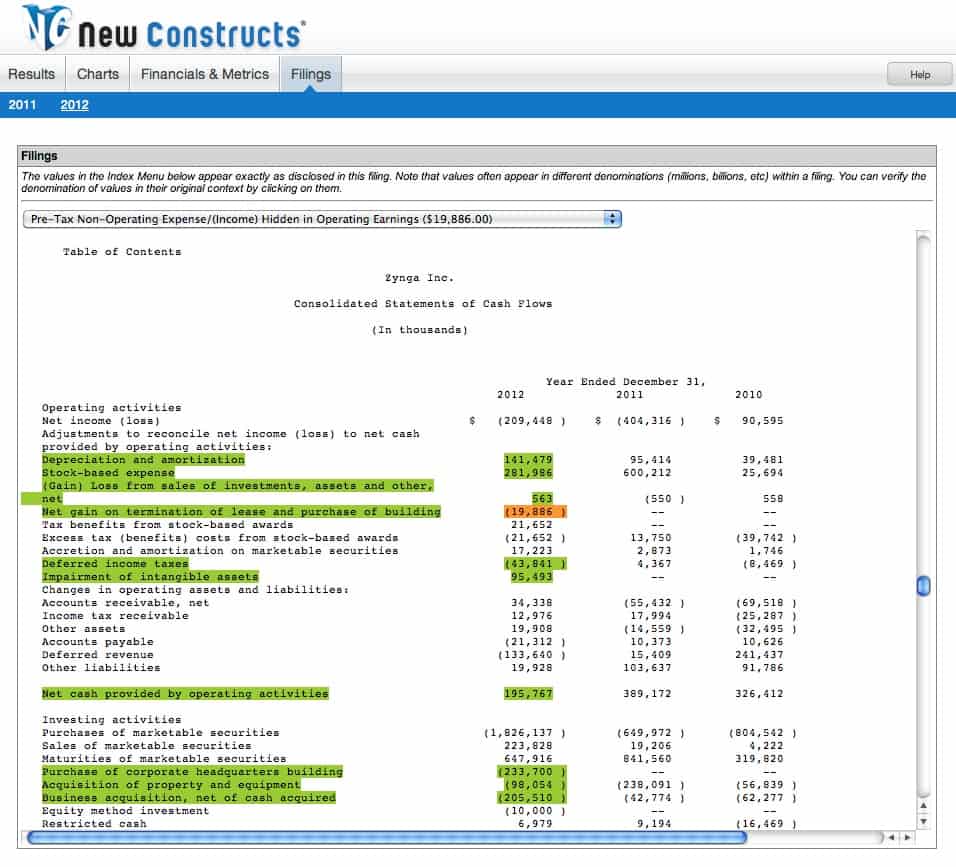

1) Unusual gains: ZNGA recorded nearly $20 million in hidden (not on income statement) gains from the termination of the lease and subsequent purchase of their headquarters building. This hidden non-operating income made ZNGA’s net loss appear nearly 10% less than without it.

{kind=link}

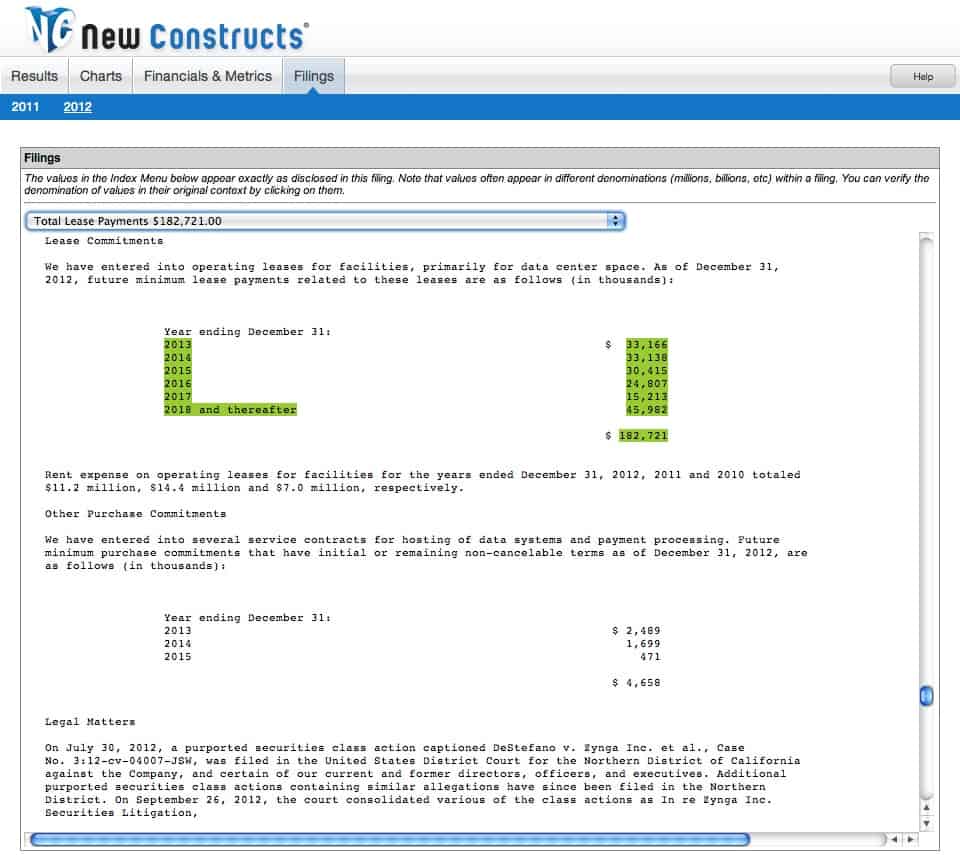

2) Off-balance sheet debt: ZNGA has nearly $183 million in operating lease commitments that it is able to hide off its balance sheet. Discounted to their present value, these leases add about $150 million to the company’s adjusted total debt, bringing it up to $250 million, or roughly 10% of total assets.

{kind=link}

3) Goodwill: ZNGA had over $210 million in goodwill (8% of total assets) on its balance sheet in 2012, an increase of nearly $120 million from the year before. That amount of goodwill can artificially inflate ZNGA’s book value. It also suggests that the company is overpaying for assets, an assertion supported by the fourth red flag.

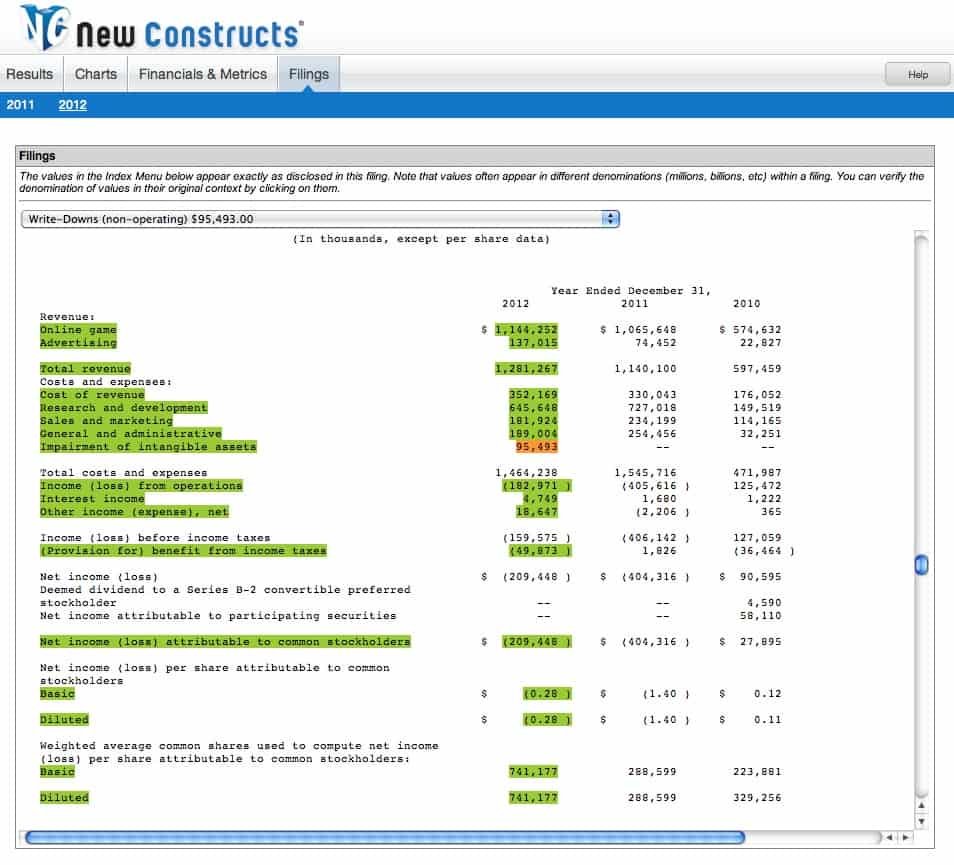

4) Asset write-downs: ZNGA was forced to take a $95 million impairment charge on intangible assets in 2012. The company has destroyed value for shareholders by paying more for assets than they’re truly worth. If this trend continues, earnings will fall further.

{kind=link}

Dangerous Valuation

Investors might be tempted to view ZNGA as a cheap stock now that it’s trading at a steep discount to its IPO price. Momentum investors might get interested given ZNGA’s 60% rise so far this year. However, trading trends are not real diligence. I recommend taking a look at the expectations baked into the stock price.

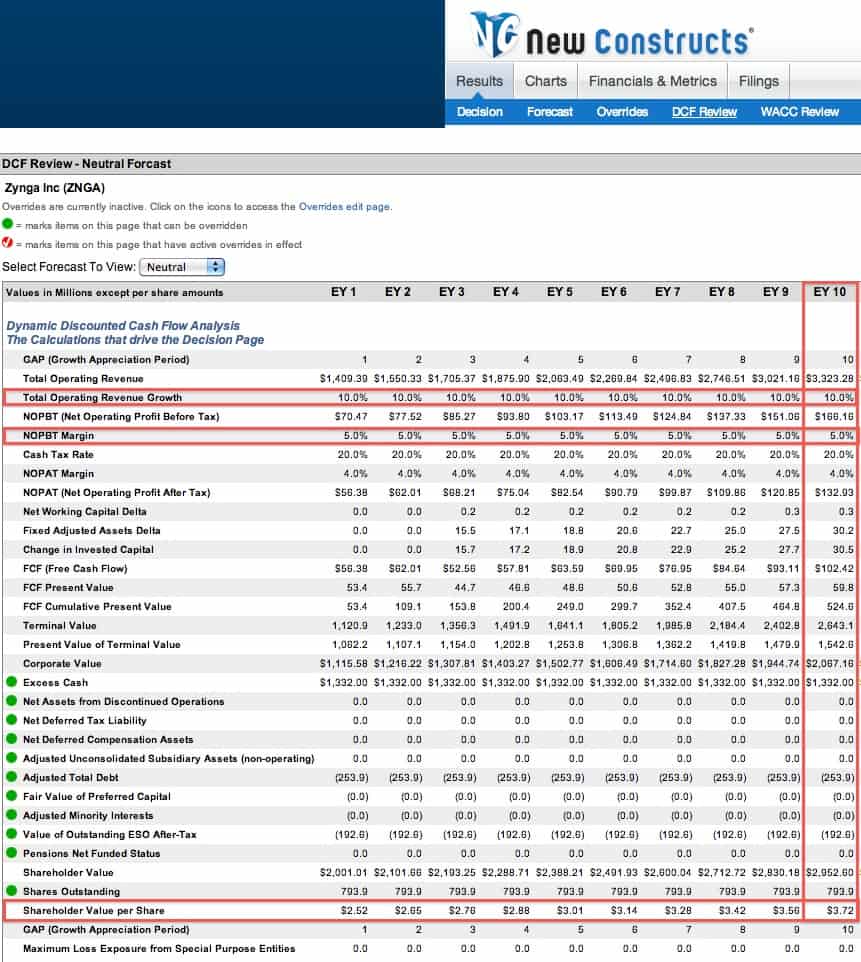

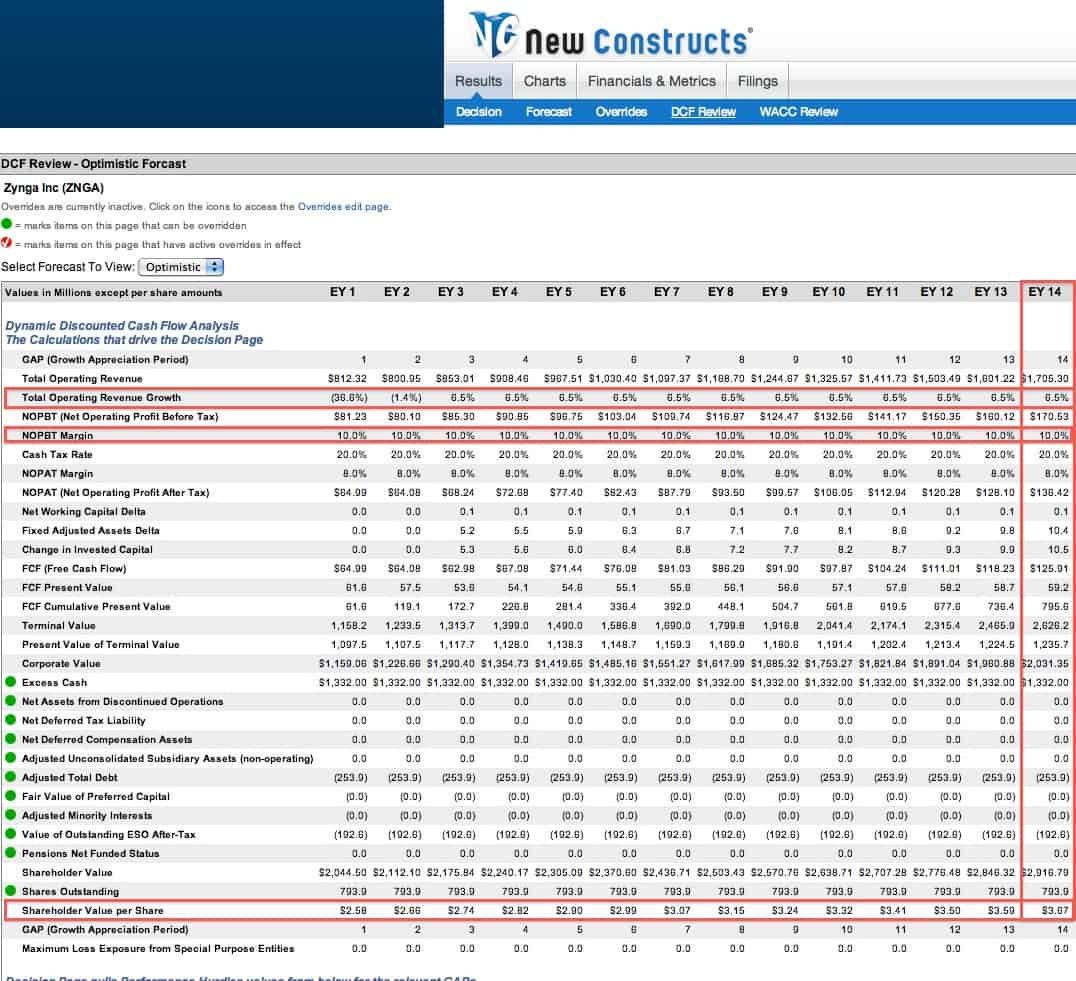

To justify its current share price of ~$3.67, ZNGA would need to grow revenue by 10% compounded annually for 10 years and improve its pre-tax margins to 5% from -8%. Such a scenario seems a bit optimistic given that consensus estimates project ZNGA’s annual revenue to decline by 37% in 2013 and another 3% in 2014.

{kind=link}

If we accept analyst projections for revenues for 2013 and 2014, the picture gets very bleak for ZNGA. Even with 10% pre-tax margins, the company would need to grow revenue by 6.5% for 12 years starting in 2015 to justify its valuation.

{kind=link}

It is hard to imagine a scenario where that level of growth and margin improvement could occur. Much has been made of a possible turnaround story at Zynga following a shakeup in its management, but it does not seem rational to bet the company can exceed the expectations for future cash flows already baked into its valuation.

Right now, the only bull case for ZNGA seems to be as a purely speculative play. If one of Zynga’s games takes off and becomes a global hit, it could see some short-term appreciation in its stock price. Long-term, however, the company should struggle to break even on a yearly basis. That $1.3 billion in cash and marketable securities is not a security blanket as the company is still burning through cash at a decent rate.

Zynga is an unprofitable company in a competitive and rapidly changing business. The stock is cheap only in comparison to its past. From a fundamental perspective, the stock is significantly overpriced and dangerous.

Avoid this ETF

Only one ETF or mutual fund allocates more than 2% of its value to ZNGA. Investors should avoid First Trust ISE Cloud Computing Index Fund (SKYY) due to its 3.6% allocation to ZNGA and Dangerous rating.

Sam McBride contributed to this article

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.