The Energy sector ranks eighth out of the ten sectors as detailed in my Sector Rankings for ETFs and Mutual Funds report. It gets my Dangerous rating, which is based on aggregation of ratings of 18 ETFs and 70 mutual funds in the Energy sector as of October 10, 2013. Prior reports on the best & worst ETFs and mutual funds in every sector are here.

Figures 1 and 2 show the five best and worst-rated ETFs and mutual funds in the sector. Not all Energy sector ETFs and mutual funds are created the same. The number of holdings varies widely (from 15 to 162), which creates drastically different investment implications and ratings. The best ETFs and mutual funds allocate more value to Attractive-or-better-rated stocks than the worst ETFs and mutual funds, which allocate too much value to Neutral-or-worse-rated stocks.

To identify the best and avoid the worst ETFs and mutual funds within the Energy sector, investors need a predictive rating based on (1) stocks ratings of the holdings and (2) the all-in expenses of each ETF and mutual fund. Investors need not rely on backward-looking ratings. My fund rating methodology is detailed here.

Investors should not buy any Energy ETFs or mutual funds because none get an Attractive-or-better rating. If you must have exposure to this sector, you should buy a basket of Attractive-or-better rated stocks and avoid paying undeserved fund fees. Active management has a long history of not paying off. Here’s the list of our top-rated Energy stocks.

Get my ratings on all ETFs and mutual funds in this sector on my free mutual fund and ETF screener.

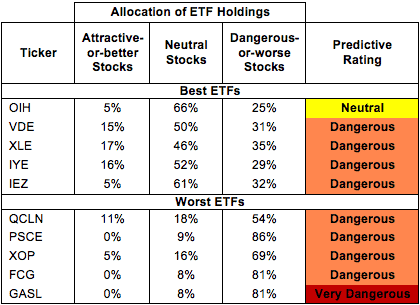

Figure 1: ETFs with the Best & Worst Ratings – Top 5

* Best ETFs exclude ETFs with TNAs less than $100 million for inadequate liquidity.

* Best ETFs exclude ETFs with TNAs less than $100 million for inadequate liquidity.

Sources: New Constructs, LLC and company filings

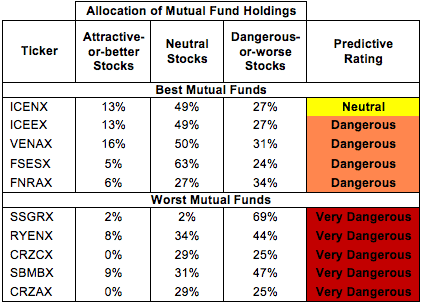

Figure 2: Mutual Funds with the Best & Worst Ratings – Top 5

* Best mutual funds exclude funds with TNAs less than $100 million for inadequate liquidity.

* Best mutual funds exclude funds with TNAs less than $100 million for inadequate liquidity.

Sources: New Constructs, LLC and company filings

World Commodity Fund (WCOMX) and ING Global Natural Resources Funds (IRGNX, IGNWX) are excluded from Figure 2 because their total net assets (TNA) are below $100 million and do not meet our liquidity minimums.

Market Vectors Oil Services ETF (OIH) is my top-rated Energy ETF and ICON Energy Funds (ICENX) is my top-rated Energy mutual fund. Both earn my Neutral rating.

Direxion Daily Natural Gas Related Bull 3x Shares (GASL) is my worst-rated Energy ETF and Saratoga Advantage Trust Energy and Cushing Renaissance Advantage Fund (CRZAX) is my worst-rated Energy mutual fund. Both earn my Very Dangerous rating.

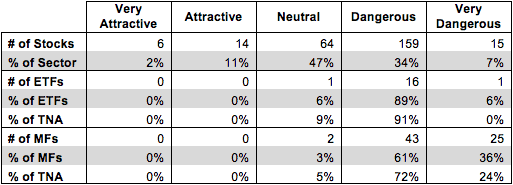

Figure 3 shows that 20 out of the 258 stocks (over 13% of the market value) in Energy ETFs and mutual funds get an Attractive-or-better rating. However, zero out of 18 Energy ETFs and zero out of 70 Energy mutual funds get an Attractive-or-better rating.

The takeaways are: mutual fund managers allocate too much capital to low-quality stocks and Energy ETFs hold poor quality stocks.

Figure 3: Energy Sector Landscape For ETFs, Mutual Funds & Stocks

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

As detailed in “Cheap Funds Dupe Investors” the fund industry offers many cheap funds but very few funds with high-quality stocks, or with what I call good portfolio management.

Investors need to tread carefully when considering Energy ETFs and mutual funds, as all of them hold too many poor stocks for me to recommend. No ETFs or mutual funds in the Energy sector allocate enough value to Attractive-or-better-rated stocks to earn an Attractive rating, and only two Energy mutual funds can manage a Neutral rating. Investors would be better off investing in individual stocks instead.

CF Industries Holdings (CF) is one of my favorite stocks held by Energy ETFs and mutual funds and earns my Very Attractive rating. CF has grown profits (NOPAT) by an impressive 60% compounded annually since 2005 and has a free cash flow (FCF) yield of almost 14%. CF also has a return on invested capital (ROIC) of 27%, which puts it in the top quintile of all companies I cover. Despite this notable profit growth over the past few years, CF is still trading at ~$207/share, which gives it a price to economic book value (PEBV) ratio of 0.5. This number implies that the market expects CF’s profits to decline by 50% and never recover. With a history of high returns on capital and high profit growth, these expectations seem too low. Investors stand to profit if they buy CF while it trades at this significant discount to economic book value.

Anadarko Petroleum (APC) is one of my least favorite stocks held by Energy ETFs and mutual funds and earns my Very Dangerous rating. APC’s profits (NOPAT) have fallen by over 4% compounded annually since 2006, and the company has a return on invested capital (ROIC) of just 5%, down from 9% in 2006. Even more troubling is the fact that APC has earned negative economic earnings for 13 of the past 15 years, including each of the past 6 years. Despite this recent history of underperformance, APC is trading at ~$94/share. To justify this share price, APC would need to grow profits by 20% each year for the next 10 years. These expectations for profit growth seem unrealistic for a company whose profits have steadily declined since 2006. Investors should risky stocks like APC.

180 stocks of the 3000+ I cover are classified as Energy stocks, but due to style drift, Energy ETFs and mutual funds hold 258 stocks.

Figures 4 and 5 show the rating landscape of all Energy ETFs and mutual funds.

My Sector Rankings for ETFs and Mutual Funds report ranks all sectors and highlights those that offer the best investments.

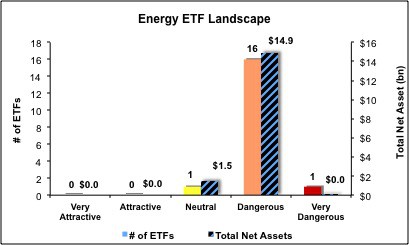

Figure 4: Separating the Best ETFs From the Worst ETFs

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

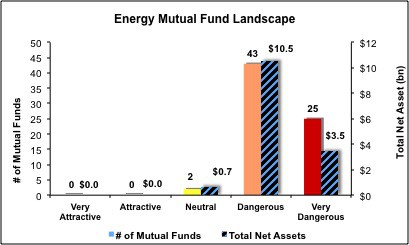

Figure 5: Separating the Best Mutual Funds From the Worst Mutual Funds

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

Review my full list of ratings and rankings along with reports on all 18 ETFs and 70 mutual funds in the Energy sector.

André Rouillard contributed to this report.

Disclosure: David Trainer owns CF. David Trainer and André Rouillard receive no compensation to write about any specific stock, sector or theme.