October’s newsletter with the 40 Most Dangerous Stocks was released to subscribers today. It will be available for purchase by the public on Monday 10/8.

October's newsletter with the 40 Most Attractive Stocks was released to subscribers today. It will be available for purchase by the public on Monday 10/8.

The guts of an ETF are its holdings. And an ETF’s guts are what drive my ETF ratings. As highlighted in Barron’s, the only truly diligent assessment of an ETF is based on its holdings.

Research on an ETF’s holdings is important because an ETF’s performance is only as good as its holdings. Therefore, if you care about performance, you care about the ETF’s holdings.

Working out makes just about everything in my life better. I have more energy, food tastes better and (at least feel as if) I look better. I even think it makes me smarter.I do not feel good about Life Time Fitness (LTM)’s stock, however. The growth expectations in the stock are much too high. And I do not believe in management’s over confident EPS guidance.

Life Time fitness CEO predicts 15% growth at best.

In my weekly Danger Zone interview, I explain how that expectation, even if it comes true, implies unrealistic member and profit growth.

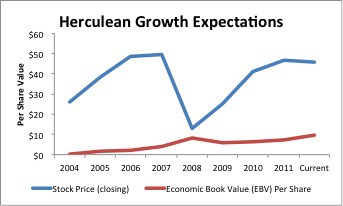

The

Smart investors consider more than just the dividend of a stock. They also consider the principal risk. If the principal risk is greater than the dividend yield then the dividend is of no real value. I see the principal risk of this stock at more than 15% with a fair value closer to $50 – after adjusting for the pension accounting shenanigans.

"New research on the performance of institutional portfolios shows that after risk adjustment, 24% of funds fall significantly short of their chosen market benchmark and have negative alpha, 75% of funds roughly match the market and have zero alpha, and well under 1% achieve superior results after costs—a number not statistically significantly different from zero."

The impact on valuation: instead of a fair value in the mid $50s, I now see it in the low $40s - about 30% lower than where the stock is today. 30% dwarfs the 4% dividend yield.

Sometimes when I analyze a stock, I am reminded of the marvels that investment bankers can do for their valuations, especially if the company is a good client. With its recent $3.7 billion acquisition of Gen-Probe, I would bet that Hologic (HOLX) made its investment bankers quite happy. Investors, on the contrary, should sell the stock and not be happy with that deal.

One of the biggest misconceptions in the investing world is that the merit of an acquisition should be judged by whether or not it is “earnings accretive”. The impact of an acquisition on a company’s accounting earnings is not indicative of its economic value to shareholders.

My last recommendation was new to the value-investing club (see Buy CSCO: A Treat For Value Investors). This week, I bring back a classic value stock: Phillip Morris (PM).

As detailed in "How To Make Money Picking Stocks", quantifying the future cash flow expectations embedded in stock prices is critical to making an informed investment decision.

My mentor, Michael Mauboussin, in his latest piece: " The Importance of Expectations – The Question that Bears Repeating: What’s Priced In?" explains more eloquently than I that the key to successful investing is to systematically distinguish between price and value – two very distinct concepts.