Converting GAAP data into economic earnings should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibilities.

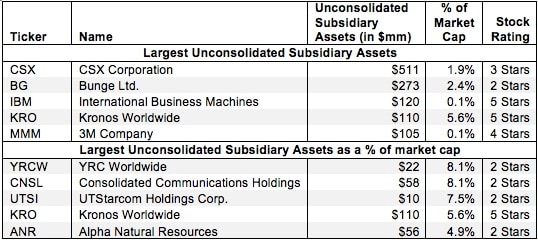

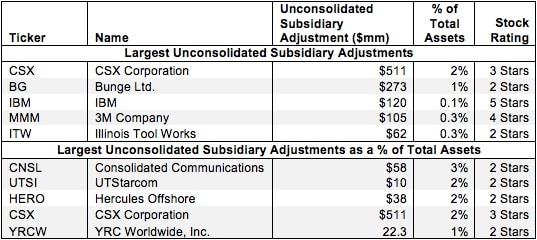

Investors who ignore unconsolidated subsidiary assets are not getting a true picture of the cash available to be returned to shareholders. By adding unconsolidated subsidiary assets one can better understand the value of the stock to shareholders. Diligence pays.

This report is one of a series on the adjustments we make to convert GAAP data to economic earnings. This report focuses on an adjustment we make to convert the reported balance sheet assets into invested capital.

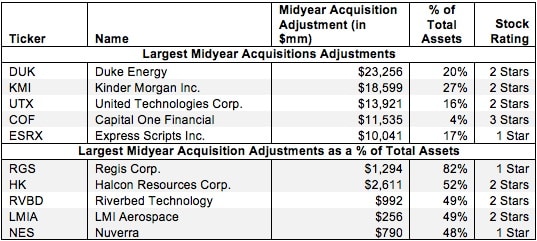

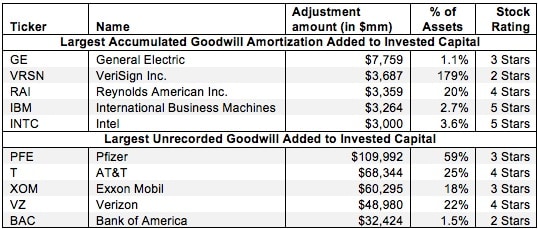

When a company makes an acquisition, the entire purchase price is added to the company’s balance sheet in the year of the acquisition along with any assumed debts or other long-term liabilities. However, the only income added to the income statement is that which occurs after the acquisition closes. In other words, the balance sheet is charged with the full price of the acquisition while the income statement only gets partially impacted.

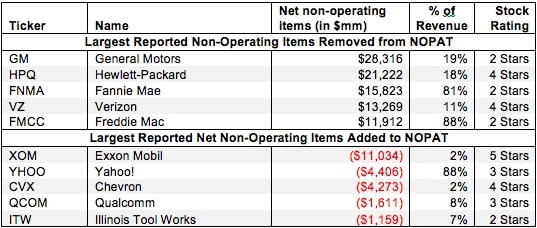

Income statement adjustments include financing items like interest expense/income, preferred dividends and minority interest income. These items are related to the financing of a company’s operations, not the operations themselves. We always calculate NOPAT on an unlevered basis.

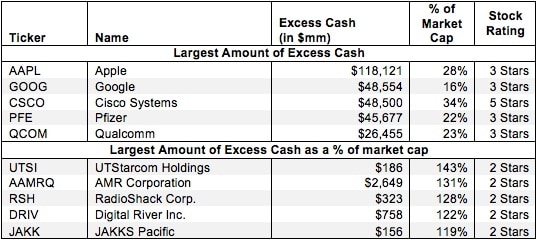

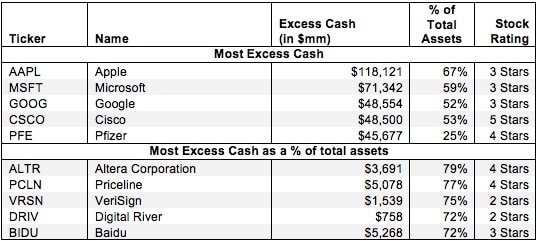

For most companies, we estimate the required amount of cash for normal business operations to be around 5% of sales. However, many companies hold cash or other liquid investments above and beyond this amount. We refer to this extra amount as excess cash. This surplus cash can be used for any number of purposes, including acquisitions, research and development, and cushioning the company against economic downturns. Excess cash is immediately available for distribution to shareholders, so we add a company’s excess cash to our calculation of shareholder value.

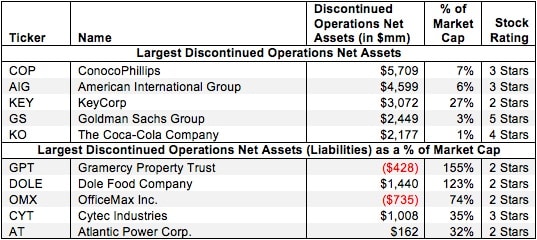

There is one last adjustment we must make involving discontinued operations: adding net assets from discontinued operations to shareholder value. Because discontinued operations are parts of a company being held for sale, the value of the net assets from these discontinued operations approximate the cash the company will receive from the sale. This cash will then be available for distribution to shareholders.

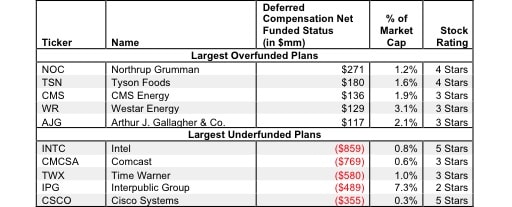

The net amount of deferred compensation is included in shareholder value. If a company has a net liability, future cash flows will be diverted to pay for that obligation. If a company has a net asset, then any future increases in the obligation will not need to be met with new contributions from the company. Instead, the company can return that cash to shareholders.

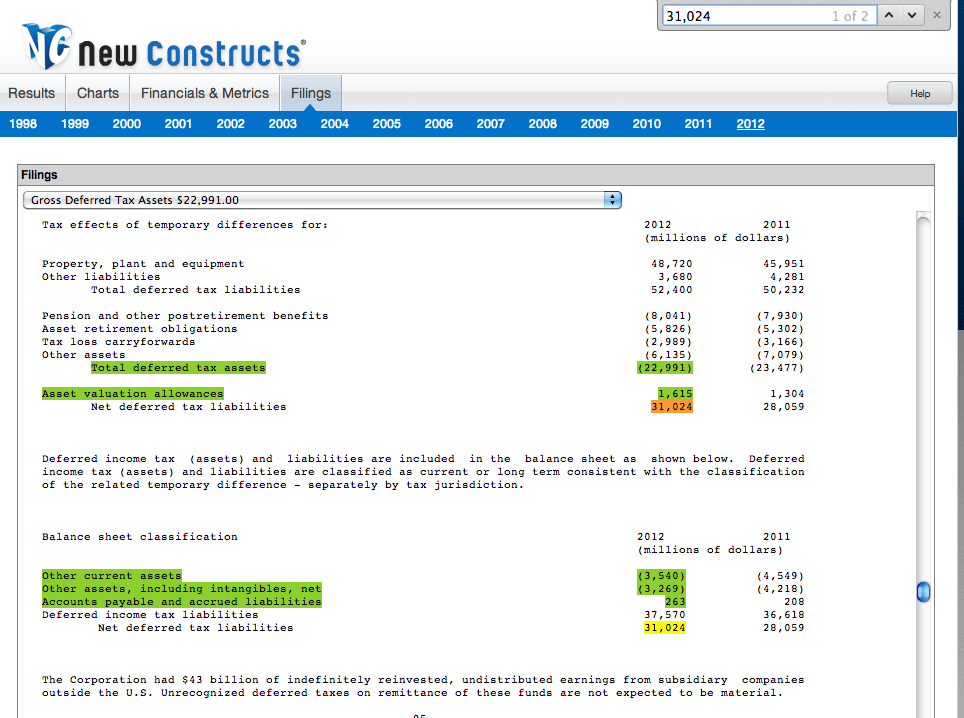

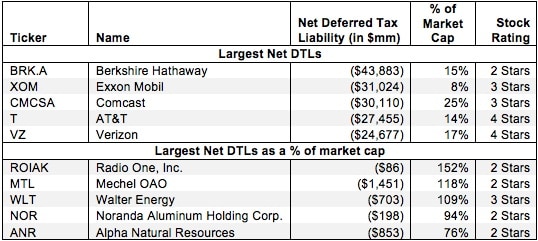

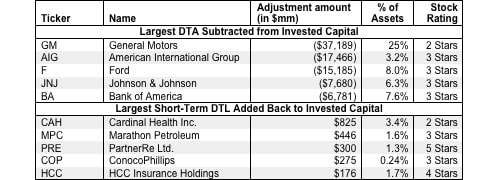

We subtract net deferred tax liabilities (DTLs minus DTAs) from our calculation of shareholder value as they are real future cash obligations that limit the amount of money available for distribution to shareholders.

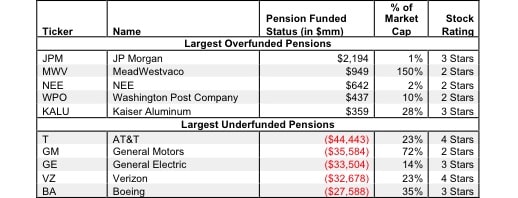

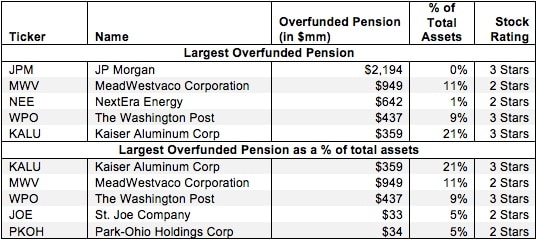

Companies with underfunded pensions will likely need to divert a greater amount of future cash flows away from shareholders to make up the funding gap. An accurate analysis of shareholder value should include the net funded status of pensions.

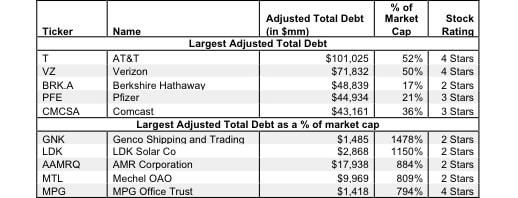

The fair value of a company’s total debt is the current amount the company would need to pay to retire the debt and settle the claims of the creditors. This fair value of debt is subtracted from shareholder value because the firm would need to settle these claims before it could return any cash to shareholders.

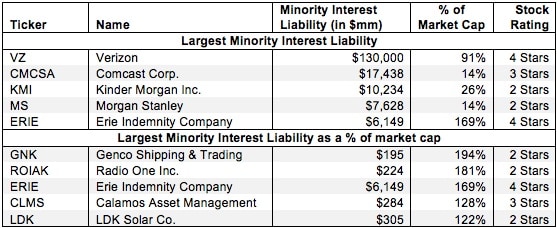

We subtract the fair value of the minority interest liability from shareholder value in our DCF model as the minority interest shareholders have the rights to that portion of the cash flows. Without careful research, investors would never know that these minority interest liabilities distort GAAP numbers.

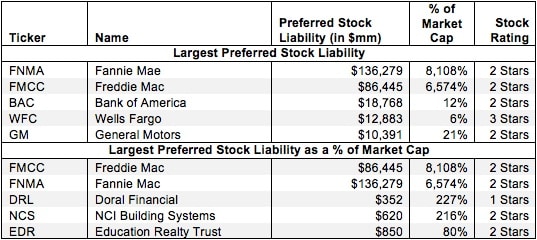

Preferred stock is a hybrid instrument that carries no voting rights but has a senior claim on assets and cash flows to common stock. Dividends usually must be paid out to preferred stock owners before common stock owners can receive any money. In the event of liquidation, preferred shareholders also have priority.

Without careful footnotes research, investors would never know the amount of employee stock options that decrease the amount of future cash flow available to shareholders by diluting the value of existing shares.

Converting GAAP data into economic earnings should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibilities.

Most companies hold some cash—or cash equivalents in the form of investments—above this required amount. Companies hold excess cash in order to cushion against economic downturns, prepare for acquisitions, or any number of other reasons. Sometimes, past profits pile up on balance sheets and are a form of excess cash. Excess cash is not needed for the operations of a company. It is removed from our calculation of invested capital.

DTAs artificially raise reported assets and do not help generate operating profit while DTLs are like a source of interest-free financing. We remove the impact of DTAs and DTLs from our calculation of invested capital to ensure the more accurate measure of a firm’s return on invested capital (ROIC).