As long as AI stays a black box, many will be hesitant to trust it. When it comes to handling people’s money, this lack of trust becomes even more pronounced.

With a track record of high profitability, significant growth opportunities, and a cheap valuation, this stock could offer significant upside for investors.

Thesis: Management can boost the market value of American Express in the amounts below[1] by aligning the firm’s strategy and performance compensation with real cash flows or what we call return on invested capital (ROIC).

While most earnings manipulation is not as blatant as the recent Valeant revelations, the fact remains that investors have to be on the lookout for earnings management at all times. To be properly vigilant, it’s important to understand why executives misstate earnings. When you understand the why, you’ll have a better sense of what you need to look for.

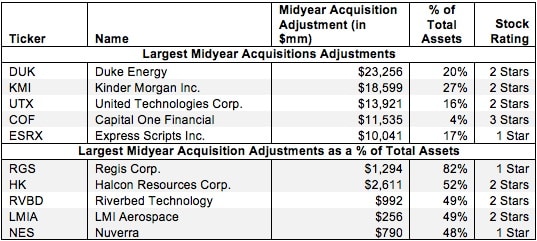

When a company makes an acquisition, the entire purchase price is added to the company’s balance sheet in the year of the acquisition along with any assumed debts or other long-term liabilities. However, the only income added to the income statement is that which occurs after the acquisition closes. In other words, the balance sheet is charged with the full price of the acquisition while the income statement only gets partially impacted.

Reported earnings don’t tell the whole story of a company’s profits. They are based on accounting rules designed for debt investors, not equity investors, and are manipulated by companies to manage earnings. Only economic earnings provide a complete and unadulterated measure of profitability.

As one financial scandal follows another, it seems the good guys are having a tougher time catching the bad guys. Recent revelations about MF Global’s ponzi scheme are another reminder of how our regulatory and oversight systems seem to let whales pass through their net.

We recommend investors short the KBW Bank ETF (KBE) and avoid or sell all other financial sector ETFs. We also rate the investment merit of the top nine financial sector ETFs.

HIDDEN GEMS:

1. Our discounted cash flow analysis shows that DFS’s current valuation (stock price of $21.80) implies that the company’s profits will decline by 40% and never grow again.

2. Economic earnings are growing faster that reported accounting earnings.

3. Free cash flow of $2.8bn or 24% of its enterprise value during the last fiscal year.