As with all things in life, building a solid investment strategy around Free Cash Flow (FCF) is not as simple as it may seem. Here are 3 rules to follow.

In our calculation of ROIC, we use a time-weighted average invested capital, to most accurately capture the capital available to a business that can be used to generate NOPAT over the course of a year.

The Financial Accounting Standards Board (FASB) introduced a new accounting standard (ASU 2016-02) that requires companies to recognize operating lease assets and liabilities on the balance sheet.

Unlike many unprofitable tech firms whose stocks have outperformed, the stock of this high-ROIC tech firm has lagged significantly over the past year. A strong competitive position and recent roll-out of new products make the profit growth expectations embedded in this stock look too low.

Invested capital turns are an important consideration in the analysis of return on invested capital (ROIC) and a key measure of balance sheet efficiency.

Our analysis of the latest 10-K and 10-Q filings for the S&P 500 shows that the GAAP earnings growth in the market has not translated to an increase in economic earnings.

Return on gross invested capital (ROGIC) (seen in Figure 1) provides additional insights into the profitability of highly-capital intensive businesses.

From yesterday’s research, analysts parsed 64 10-K filings and collected 8,054 data points. In total, they made 1,318 forensic accounting adjustments with a dollar value of $55 billion. Analyst Allen L. Jackson found an unusual item yesterday in Alcoa’s (AA) 10-K.

As tireless advocates for the importance of Return on Invested Capital (ROIC), we’ve been encouraged to see a growing appreciation for the metric. Unfortunately, many investors may be relying on flawed calculations of ROIC.

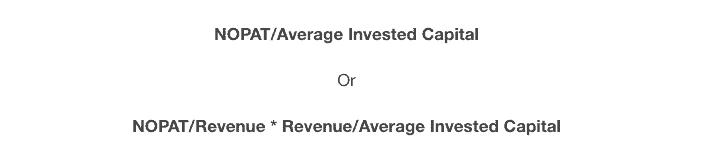

We calculate invested capital in two mathematically equivalent ways: financing and operating approach. Figure 1 shows the basic calculations. On page 2, we share the complete calculations for specific companies.

In this webinar, we provide details and models showing how to calculate Invested Capital and how it relates to Net Operating Profit After Tax (NOPAT) and return on invested capital (ROIC).

Analysts and investors tend to spend very little time on Goodwill when looking at financial statements. In reality, Goodwill is an important number to keep an eye on. Since it reflects the money paid for acquisitions above the market value of the acquired company, it can signal overpayment, reckless spending, and the potential for damaging write-downs in the near future.

Watch David Trainer explain the importance of understanding how much capital has truly gone into a business, and the adjustments we make to calculate this metric.

The second step to gauge the value of a company is to determine the sum of all cash that has been invested in a company over its life without regard to financing form or accounting name. We call this Invested Capital.

On August 27th, I met with my fellow members of the FASB’s Investor Advisory Committee (IAC) to discuss the proposed treatment of operating leases on the balance sheet by the Financial Accounting Standards Board (FASB).

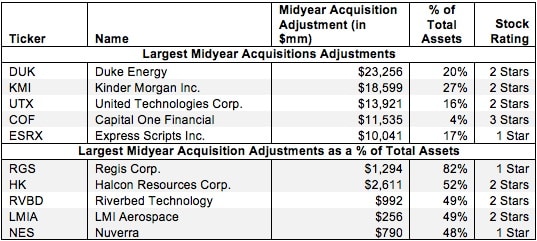

When a company makes an acquisition, the entire purchase price is added to the company’s balance sheet in the year of the acquisition along with any assumed debts or other long-term liabilities. However, the only income added to the income statement is that which occurs after the acquisition closes. In other words, the balance sheet is charged with the full price of the acquisition while the income statement only gets partially impacted.