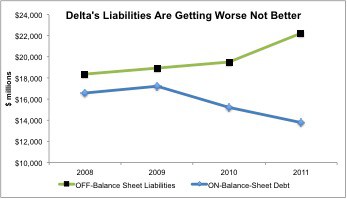

The new operating lease rule is not perfect. These companies use unusually high discount rates to reduce and, perhaps, understate their reported operating lease burden.

Investment Analyst Sam McBride sat down with Chuck Jaffe of Money Life to talk about our Danger Zone pick this week: Danger Zone: Misleading Operating Lease Discount Rates.

Investors that don’t pay attention to this accounting rule change are taking on unnecessary risk by mistaking an upcoming change as a fundamental change in these businesses.

Why are earnings misstatements so contagious? Learn why these misstatements occur and warnings signs of when a company may be likely to partake in the manipulation of earnings in this special report.

Last week, the Financial Accounting Standards Board (FASB) voted to update standards on operating lease accounting that would force companies to record as much as $2 trillion worth of lease obligations on their balance sheets.

On August 27th, I met with my fellow members of the FASB’s Investor Advisory Committee (IAC) to discuss the proposed treatment of operating leases on the balance sheet by the Financial Accounting Standards Board (FASB).

RAD is up against the ropes right now. The company has to contend with larger, more efficient competitors, significant debt, and declining sales. Don’t be fooled by the 150% growth in the share price this year. RAD is much worse off than its stock suggests.

Red flags:

1. Misleading earnings: BJRI reported a $3mm increase in GAAP earnings while our model shows economic earnings declined by $2mm (a difference of $5mm or nearly 40% of reported net income) during the last fiscal year.

2. Very dangerous valuation: stock price of $34 implies BJRI must grow its NOPAT at over 20% compounded annually for 15 years. A 15-year growth appreciation period with a 20%+ compounding growth rate sets expectations for future cash flow performance quite high. Historical growth rates are much lower.

3. Free cash flow was -$83mm or -11% of the company’s enterprise value last year.

4. Off-balance sheet debt of $265mm: 79% of net assets and 25% of market value.

5. Outstanding stock option liability of $44mm or 5% of current market value.

We went on record that investors should short SBUX on 11/6/2006 when the stock was close to $38 per share. Click here to see the Fortune Article. The stock did not look attractive to us until 2 years (11/18 – 11/20/08) later when it was under $8, and that for only about 3 days. And ever since we have had a Neutral or Dangerous Rating on the stock.

The first in a series of upcoming reports on Red Flags and Hidden Gems, we published our Red Flag Report on Off-Balance Sheet Debt. This report delivers:

1. Measurement of the impact of the operating lease accounting loophole on the entire stock market and all 3000 companies we cover.

2. Explanation of exactly how the off-balance sheet debt from operating leases affect economic earnings.

Rite Aid Corp (RAD) gets a Dangerous Rating because of these RED FLAGs:

1. Very Expensive valuation: current stock price implies the company will grow revenues and NOPAT at 6% compounded annually for the next 15 years while also more than doubling ROIC from 6.1% to 13.7% within the same time frame.

2. Off Balance-Sheet debt: of $5,502mm or 93% of "Reported" Net Assets

3. Asset-write-offs: $3,417mm or 58% of "Reported" Net Assets