Millions of professional investors will soon see over $3 trillion in new debt added to corporate balance sheets, which will affect some stocks and sectors much more than others.

The Financial Accounting Standards Board (FASB) introduced a new accounting standard (ASU 2016-02) that requires companies to recognize operating lease assets and liabilities on the balance sheet.

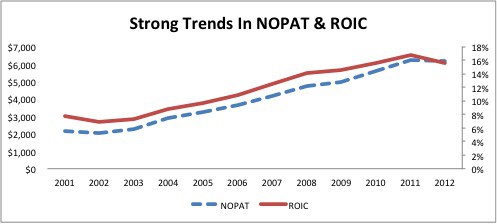

Last month, Fortune released its list of the top 50 businesspeople of the year. The recognition these CEO’s are receiving shows that the market cares about ROIC, even if many investors aren’t explicitly talking about it.

Why are earnings misstatements so contagious? Learn why these misstatements occur and warnings signs of when a company may be likely to partake in the manipulation of earnings in this special report.

DNKN’s illusory growth in accounting earnings has driven the stock up nearly 40% while the S&P 500 is up only about 20% over the past year. Our diligence reveals that while reported earnings are up, DNKN’s economic earnings are in decline. Future growth expectations are overblown as well because the company’s plans to expand outside of the Northeast pit it against formidable, entrenched competitors.

We applaud the Financial Accounting Standards Board's (FASB) latest proposal to change the way leases are reported. The new rules would make only the shortest-term operating leases exempt from being recorded on the balance sheet.

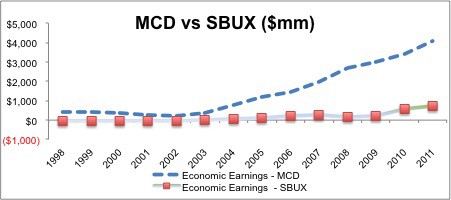

The stock market is giving MCD no credit for the company’s proven track record of value creation and strong growth potential. Instead, the market predicts MCD’s profits will permanently drop. I think it is pretty clear the market’s expectations are too low for MCD. Investors should take advantage.

When McDonalds (MCD) made my Most Attractive Stocks list this month, I must admit I let out a small cheer. This company is one of the better-run businesses in the world. I have long eyed the stock in hopes that it would get cheap enough to dig into and now it has.

When stocks are priced for perfection as SBUX is, they are very risky. Just look at today's 10%+ drop in SBUX shares in a market that is up 1%.

My regular readers know that I have, for a while, warned investors that SBUX was overpriced and due for a correction. See "Get Off the SBUX Bandwagon Before It Crashes".

Be wary of advice from the bandwagon riders. They care more about getting more people in the bandwagon than anything else.

The Starbucks (SBUX) bandwagon is a big one. I am not on it.

We went on record that investors should short SBUX on 11/6/2006 when the stock was close to $38 per share. Click here to see the Fortune Article. The stock did not look attractive to us until 2 years (11/18 – 11/20/08) later when it was under $8, and that for only about 3 days. And ever since we have had a Neutral or Dangerous Rating on the stock.